In an audacious move that could dramatically improve the financial health of millions of Americans, the Biden administration proposed a new rule on Tuesday to ban medical debt from appearing on credit reports.

Announced jointly by Vice President Kamala Harris and Consumer Financial Protection Bureau (CFPB) Director Rohit Chopra, this sweeping change aims to address one of the most persistent and devastating financial burdens faced by everyday citizens in this country.

By removing the threat of damaged credit for those already grappling with astronomical healthcare costs, the administration is taking a significant step towards restoring financial stability and dignity for the most vulnerable among us.

The Burden of Medical Debt

A Uniquely American Problem

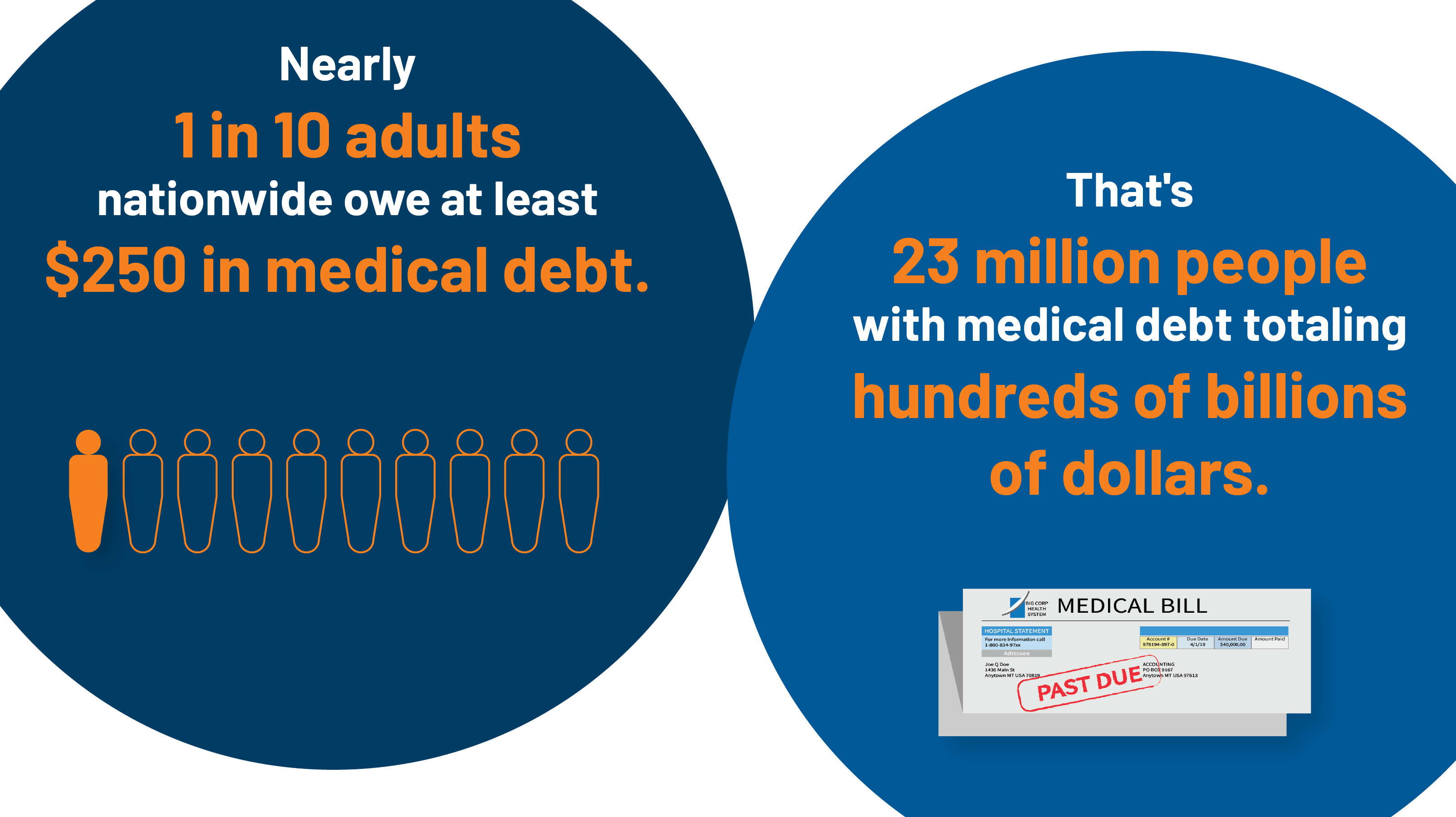

Medical debt is a scourge that afflicts an estimated 100 million people in the United States, with 15 million carrying a staggering $49 billion in unpaid bills that have gone to collections.

As Neale Mahoney, an economist at Stanford University who has studied the effects of medical debt throughout his career, astutely observes, “More than any other form of financial distress or debt, medical debt is the result of bad luck, not bad behavior. Nobody chooses to get sick, but we end up with a mess of medical bills.”

This distinction is crucial.

Unlike other forms of debt that may result from irresponsible spending or poor financial decisions, medical debt is often an unavoidable consequence of falling ill or suffering an accident in a country with a broken healthcare system.

It is a problem that disproportionately affects people of color, who face higher rates of chronic illness and persistent wealth gaps compared to white Americans.

Real-Life Struggles and Tough Choices

Behind the staggering statistics are countless personal stories of hardship and sacrifice.

Take Lexi Coburn, who at just 23 years old and uninsured, found herself with a $425 emergency room bill for treatment of early onset arthritis.

Unable to pay, she watched helplessly as her medical debt ballooned to over $2,300, wreaking havoc on her credit score and making it nearly impossible to secure a car loan.

Or consider Linda Davis, a 61-year-old resident of Grand Rapids, Michigan, who estimates her medical bills to be between $45,000 and $50,000.

“There’s no way on God’s green earth I could pay all those medical bills,” Davis laments.

“Even if I paid a small amount every month, I wouldn’t live long enough to pay them all.”

These are not isolated cases, but rather emblematic of a pervasive problem that forces countless Americans to choose between their health and their financial well-being.

DonnaMarie Woodson, a cancer survivor from Charlotte, N.C., poignantly recalls delaying care for a year while uninsured, “not wanting to get into medical debt.”

When she finally scheduled her screenings after the passage of the Affordable Care Act, she discovered she had late-stage colon cancer and breast cancer.

Inside the Game-Changing Proposal

Key Provisions and Expanded Protections

The proposed rule is a multi-faceted approach to tackling the issue of medical debt and its impact on credit scores.

At its core, it would prohibit credit reporting agencies from including medical debts—including those from dental bills—on consumer credit reports.

This ban extends to lenders, who would no longer be permitted to factor medical debt into their decisions about a person’s creditworthiness.

Additionally, the rule would bar lenders from using medical devices as collateral for loans, a practice that can lead to the repossession of essential items like wheelchairs and prosthetic limbs if the debt goes unpaid.

These protections represent a significant expansion of the voluntary actions taken by major credit bureaus and scoring companies in 2023, which removed paid bills and those under $500 from credit reports.

| Key Provision | Impact |

|---|---|

| Ban medical debt from credit reports | Prevents damage to credit scores due to unpaid medical bills |

| Prohibit lenders from factoring medical debt into credit decisions | Ensures access to credit is not unfairly restricted |

| Bar use of medical devices as loan collateral | Protects essential equipment from repossession |

Expected Rollout in Early 2025

While the proposed changes offer hope for millions, they won’t take effect overnight.

Administration officials plan to review public comments on the proposal through the remainder of 2024, with the goal of issuing a final rule in early 2025.

Once enacted, the rule would not only prevent future medical debts from appearing on credit reports but also remove any existing ones.

It’s important to note that while the debts would be banned from credit reporting, patients would still owe the money and potentially face other collection efforts, such as lawsuits.

The rule also wouldn’t apply to medical debts paid via credit card, which would continue to appear on credit reports.

Debts Owed But No Longer Reported

A key distinction of the proposed rule is that while it would prohibit medical debts from being reported to credit agencies, it does not eliminate the debts themselves.

Patients would still be obligated to pay their outstanding balances, and hospitals, physicians, and other providers could pursue other collection tactics, including legal action, to recoup the money owed.

However, one significant exception to the reporting ban involves medical debts paid using credit cards, including specialized medical credit cards like CareCredit.

These debts would continue to appear on credit reports, as they are considered traditional credit card debt rather than medical debt.

This nuance highlights the importance of understanding the various ways in which medical expenses can impact one’s financial health.

Despite these caveats, the removal of medical debt from credit reports represents a seismic shift in how the financial burden of healthcare is handled in the United States.

By decoupling medical misfortune from credit worthiness, the Biden administration is taking a crucial step towards ensuring that a health crisis doesn’t also become a financial catastrophe.

Unlocking Opportunity for Millions

A Clean Slate for Credit Scores

For the 15 million Americans currently carrying $49 billion in medical debt on their credit reports, the proposed rule offers the promise of a fresh start.

Research from the CFPB suggests that some consumers could see their credit scores increase by as much as 20 points once medical debts are removed from their reports.

This boost in creditworthiness could translate into tangible benefits, such as increased access to mortgages, auto loans, and other forms of credit.

In fact, the CFPB estimates that the rule change could lead to the approval of 22,000 additional mortgages annually, as lenders would no longer be able to factor medical debt into their decisions.

For many Americans, this could mean the difference between renting and owning a home, or between a subprime loan and a more affordable one.

The potential impact on credit scores is not just a matter of numbers, but of real-life opportunities.

A higher credit score can open doors to better housing, more reliable transportation, and even job prospects, as some employers use credit checks as part of their hiring process.

By giving millions of Americans a clean slate, the Biden administration is not only addressing a financial burden but also a barrier to economic mobility.

Removing Barriers to Economic Mobility

Vice President Kamala Harris put it succinctly: “No one should be denied access to economic opportunity simply because they experienced a medical emergency.”

Yet for too many Americans, that is precisely what happens when medical debt appears on their credit reports.

A low credit score can be a formidable obstacle to financial stability and upward mobility.

It can make it harder to secure a loan for a car to get to work, to rent an apartment in a safe neighborhood, or to qualify for a mortgage to buy a home.

In some cases, it can even prevent someone from getting a job, as certain employers view poor credit as a red flag.

By banning medical debt from credit reports, the Biden administration is sending a clear message that a person’s health should not determine their financial future.

This move has the potential to unlock opportunities for millions of Americans who have been held back by the weight of medical debt, giving them a chance to pursue their dreams and build a better life for themselves and their families.

Stakeholder Reactions and Concerns

Hospitals and Debt Collectors Push Back

While consumer advocates have celebrated the proposed rule as a game-changer for Americans burdened by medical debt, not everyone is thrilled with the prospect of change.

Hospital leaders and representatives of the debt collection industry have warned of unintended consequences, arguing that the rule could have a “broad negative impact” on businesses, healthcare providers, patients, and consumers.

One major concern is that by removing the threat of credit reporting, the rule could lead to an increase in unpaid medical bills.

If patients face fewer repercussions for not paying their debts, critics argue, they may be less likely to prioritize those payments.

This, in turn, could put additional financial strain on hospitals and other healthcare providers, who rely on patient payments to cover their costs.

Another worry is that the rule change could prompt more hospitals and physicians to require upfront payment before delivering care, a practice that could disproportionately impact low-income patients and those without insurance.

“The rule, if finalized, would fundamentally alter the U.S. credit-based economy as it is today in terms of reduced consequences for not paying your bills, which in turn will reduce access to credit and health care for those that need it most,” warned ACA CEO Scott Purcell.

Consumer Advocates Cheer and Call for More

On the other side of the debate, consumer advocates and patient rights groups have hailed the proposed rule as a major victory in the fight against predatory debt collection practices.

Organizations like the National Consumer Law Center (NCLC) and Community Catalyst, which have long pushed for stronger federal protections for patients, see the move as a crucial first step towards addressing the broader issue of medical debt in America.

“This is a really big deal,” said Mona Shah, a senior director at Community Catalyst.

“We know empirically that the repayment rates are incredibly low for medical debt, and so it’s already the case that people aren’t really paying it down.

So I don’t think this policy change is going to change the behavior that dramatically.”

At the same time, these groups acknowledge that banning medical debt from credit reports is just one piece of a larger puzzle.

They are also calling on the federal government to take additional steps, such as prohibiting nonprofit hospitals from selling patient debt to third-party collectors or denying care to those with past-due bills.

These practices remain widespread across the country, despite the harm they can cause to vulnerable patients.

CFPB Defends Approach and Impact

Amid the swirling debate, CFPB Director Rohit Chopra has remained steadfast in his defense of the proposed rule.

In response to concerns about an increase in defaults, Chopra noted that patients will still face other penalties for not paying their bills, such as lawsuits and collection actions.

“There are plenty of ways that people get penalized for not paying their bills,” he told ABC News.

“I just don’t want to see the credit reporting system be weaponized against people who already paid them.”

Chopra also pointed to CFPB research showing that medical debt is a poor predictor of a person’s overall creditworthiness.

Unlike other types of debt, such as credit card balances or auto loans, medical debt does not necessarily reflect a consumer’s ability or willingness to repay their obligations.

In many cases, it is simply a reflection of bad luck or a flawed healthcare system.

“Our research shows that medical bills on your credit report aren’t even predictive of whether you’ll repay another type of loan,” Chopra explained.

“That means people’s credit scores are being unjustly and inappropriately harmed by this practice.”

By removing medical debt from the equation, the CFPB hopes to create a fairer, more accurate credit reporting system that doesn’t penalize people for seeking the care they need.

One Piece of a Larger Puzzle

Confronting the Roots of the Crisis

While the proposed rule has the potential to provide relief for millions of Americans, experts caution that it does not address the underlying causes of the medical debt crisis.

As Stanford economist Neale Mahoney notes, the rule is not a cure-all for the “uniquely American problem” of gaps in the healthcare system that leave many people vulnerable to financial ruin.

“Nobody chooses to get sick, but we end up with a mess of medical bills,” Mahoney told The New York Times.

The root of the problem, he and other experts argue, lies in a fragmented and often inadequate health insurance system that leaves too many people unprotected.

Lack of coverage, high deductibles, and narrow provider networks can all contribute to the accumulation of medical debt, even for those who have insurance.

Addressing these systemic issues will require a multi-faceted approach that goes beyond credit reporting.

This could include expanding access to affordable, comprehensive health insurance, increasing funding for hospitals that serve low-income communities, and reforming the billing and collection practices of healthcare providers.

While the Biden administration’s proposed rule is a significant step forward, it is just one part of a larger effort to ensure that no American has to choose between their health and their financial well-being.

Expanding State-Level Protections

As the federal government moves to ban medical debt from credit reports, a growing number of states are taking their own steps to protect consumers.

In recent months, Colorado, New York, and California have all enacted legislation to restrict the reporting of medical debt and increase the amount of charity care that hospitals must provide to low-income patients.

These state-level initiatives reflect a growing consensus that medical debt is a unique and pressing problem that requires targeted solutions.

By limiting the ability of hospitals to pursue aggressive collection tactics, and by mandating more generous financial assistance policies, states hope to provide a safety net for patients who might otherwise fall through the cracks.

The Biden administration has also urged more states to follow suit, calling on them to limit hospital debt collection practices and expand access to charity care.

This kind of coordinated effort, with action at boththe federal and state levels, could create a more comprehensive and effective response to the medical debt crisis.

A Step Forward, But Miles to Go

The proposed rule to ban medical debt from credit reports is a significant and transformative step towards alleviating the burden of healthcare costs on American families.

By removing this debt from the calculation of credit scores, the Biden administration is giving millions of people a chance to regain their financial footing and access opportunities that might otherwise be closed to them.

However, it is important to recognize that this rule, while groundbreaking, is not a panacea for the deeper problems plaguing the American healthcare system.

Medical debt is a symptom of a larger crisis, one that leaves too many people uninsured, underinsured, or faced with bills they cannot hope to pay.

Solving this crisis will require a sustained and multi-faceted effort, one that addresses the root causes of medical debt and ensures that everyone has access to the care they need without risking financial ruin.

In the meantime, the proposed rule offers hope and relief to millions of Americans who have been struggling under the weight of medical debt.

It is a recognition that no one should have to pay the price for being sick or injured in their credit score, and that a just and humane society must find ways to separate the cost of care from the consequences of credit.

As Berneta Haynes of the National Consumer Law Center put it, “Even if they eventually pay it, it’s likely to show up on their credit report before they’re able to do it.”

This rule ensures that will no longer be the case.

Setting the Stage for 2024

A Key Piece of Biden’s Economic Agenda

The timing of the proposed rule is no accident.

With the 2024 presidential election on the horizon, the Biden administration is keen to demonstrate its commitment to reducing costs and improving financial security for American families.

The medical debt rule is just one part of a broader economic agenda that includes everything from student loan forgiveness to expanded child tax credits.

By taking on an issue that affects so many Americans, and that resonates deeply with those who have experienced the stress and trauma of medical debt, Biden is positioning himself as a champion of the middle class and a defender of the vulnerable.

The rule’s potential impact on credit scores and access to loans could be a powerful talking point on the campaign trail, a concrete example of how the administration is working to create opportunity and prosperity for all.

At the same time, the rule’s focus on medical debt specifically taps into a growing sense among voters that the healthcare system is broken and in need of major reform.

By acknowledging the unique burden of medical debt and taking steps to address it, Biden is signaling that he understands the challenges facing American families and is willing to take bold action to solve them.

Giving Americans a Seat at the Table

As impactful as the proposed rule could be, it is not yet a done deal.

The Biden administration has opened a public comment period, running through August 12, to allow individuals and organizations to weigh in on the proposal.

This is a critical opportunity for Americans to make their voices heard and to shape the final contours of the rule.

Consumer advocates and patient rights groups are already mobilizing their members to submit comments in support of the rule, arguing that it is a necessary and overdue step towards protecting vulnerable patients from the worst excesses of the medical debt collection system.

They are also using the comment period to push for additional measures, such as limits on hospital lawsuits against patients and mandatory financial assistance for low-income individuals.

On the other side, hospitals, debt collectors, and credit reporting agencies are likely to mount a vigorous opposition campaign, warning of unintended consequences and pushing for a narrower rule or no rule at all.

The outcome of this debate will depend in large part on the level of public engagement and the persuasiveness of the arguments on both sides.

Restoring Financial Stability and Dignity

At its core, the proposed rule to ban medical debt from credit reports is about more than just a number on a page.

It is about restoring financial stability and dignity to millions of Americans who have been unfairly penalized for the crime of getting sick or injured.

Medical debt is a uniquely pernicious form of financial burden, one that strikes without warning and can quickly spiral out of control.

It can force people to make impossible choices between paying for food and rent or covering the cost of a necessary procedure.

It can trap families in a cycle of poverty and stress, as unpaid bills lead to damaged credit, which in turn leads to higher interest rates, rejected loan applications, and even lost job opportunities.

By removing this debt from credit reports, the Biden administration is giving Americans a chance to break free from that cycle and to rebuild their financial lives.

It is a recognition that no one should have to bear the double burden of illness and economic ruin, and that a just society must find ways to decouple the two.

Ultimately, the fight against medical debt is about more than just credit scores or loan approvals.

It is about the kind of country we want to be, one where a trip to the hospital doesn’t have to mean a lifetime of financial struggle, and where everyone has the opportunity to pursue their dreams and build a better future for themselves and their families.

The proposed rule is a crucial step in that direction, and a powerful reminder of the difference that bold, compassionate policy can make in the lives of ordinary Americans.