We know you’re looking for the latest statistics on chip shortage, and we’ve got you covered. We’ve compiled a list of chip shortage statistics that will help you get a better idea of the impact of this issue.

We know how painful it can be to not have access to relevant information. That’s why we’re here: to help you find exactly what you need when you need it. Our list has been curated by our team of researchers, who combed through hundreds of articles and studies to find only the most important stats so that you don’t have to spend hours doing research yourself.

You’ll find everything from estimates on how many chips are in circulation right now to predictions about how long this shortage will last—and everything in between!

So check out our list today, and start getting the answers you need about chip shortage statstics!

Semiconductor Market Statistics

1. Worldwide semiconductor industry revenue is set to grow by 13.7%

(IDC)

The Worldwide Semiconductor Tech and Supply Chain Intelligence report from IDC demonstrates a potential growth in semiconductor revenue by 13.7% by the end of 2022. This will accelerate the market value to around $661 billion, compared to 2021’s $582 billion.

Looking at demand by industry, IDC notes that need for chip products was greatest in the automotive (26.7%) and industrial (30.2%) sectors throughout 2021.

Examining the future, IDC forecasted that five-year CAGR in the semiconductor space would grow by around 4.93% between 2021 and 2026.

2. Since 1996 chips have seen growth of 35-60% four times

(Deloitte)

Examining the evolution of the chip market and the changing demand for chip technology over the years, Deloitte found there have been various significant periods of growth and decline. Since 1996, demand for chips has increased by between 35 and 60% four separate times.

However, the demand for chips have also dropped by 15-50% on five occasions.

3. Samsung is the world’s biggest producer of semiconductor chips

(IDC)

According to IDC’s report in 2021, Samsung stood out in the report as the number one producer and seller of semiconductor solutions. The company achieved a revenue of $75.8 billion in 2021, compared to $57.7 billion in 2020, marking a 31.1% increase.

Other companies in the “top 5” spots for the report included Qualcomm, Micron, SK Hynix, and Intel. IDC noted that the top 10 companies in the industry were currently responsible for holding around 58% of the market share, while the top 20 companies were responsible for around 76%.

4. Global semiconductor sales increased 18% between May 2021 and 2022

(WSTS)

A report released by the World Semiconductor Trade Statistics organization found global sales of semiconductor chips averaged around $51.8 billion in the Month of May for 2022. This represented an overall increase of 18% from May 2021, and a 1.8% increase from April 2022.

Examining where the majority of sales were taking place, the report found between April 2021 and May 2022, the Americas saw an increase of 36.9%, while Japan saw a boost of 19.8%. Europe followed close behind at 16.1% with its sales increase.

5. The US currently leads the world in developing and selling semiconductors

(TS Lombard)

According to analytics released by TS Lombard, the US currently leads the world in the development and sale of semiconductors, accounting for around 45-50% of billings worldwide. However, the Americas are far from the top of the list when it comes to producing these products.

The majority of chip manufacturing is done in Asia, with Korea and Taiwan accounting for around 70% of memory chip output, and 83% of global processor chip production.

Taiwan is particularly strong in the foundry market. The company “TSMC”, or Taiwan Semiconductor Manufacturing Co accounted for 54% of the global foundry revenue in 2021 according to the report.

Chip Supply and Demand Statistics

6. There are 470 semiconductor companies, but only 31 fabrication companies worldwide

(Accenture)

In many reports around the chip shortage, lack of access to fabrication solutions has emerged as a significant problem in meeting demand. Unfortunately, according to an Accenture report, semiconductor companies have a limited number of fabrication companies to choose from.

As of 2021, there were 470 semiconductor companies active around the world, but only 31 fabrication companies delivering wafers for the ecosystem. Even the packaging engineering options are extremely low, with only around 101 companies worldwide.

7. The demand for chips for AI is expected to grow at over 50% for the next few years

(Deloitte)

Exploring the rapid changes in supply and demand for the chip landscape, Deloitte notes that the demand for chips for AI solutions, particularly inference and training for machine learning, will grow at a rate of around 50% per year for the next few years.

This makes sense when we look at accompanying studies from brands like IDC, who found global shipments of PCs were increasing by around 55.2% between the years of 2020 and 2021.

PC shipments still only reached around 84 million worldwide in the first quarter of 2021, however, which indicates a slight decline from the fourth quarter of 2020.

8. Demand for chips was 17% higher in 2021 than in 2019

(Commerce.gov)

According to the Request for Information report supplied by the US Commerce Department, demand is far outweighing supply in the chip and semiconductor industry.

Respondents to the study, such as manufacturers like NVIDIA and Intel, say they don’t believe this issue will disappear any time soon.

The report showed median demand for chips was around 17% higher in 2021 compared to 2019, and buyers are not able to access as many chips as they would like. The main problem highlighted in assessing the gap between supply and demand is a need for additional fabrication capacity.

However, the chip manufacturers also said they were struggling with material and assembly processes, testing, packaging capacity, and more.

9. Electric vehicles, smartphones and personal computers are some of the biggest products increasing demand for chip production

(S&P Global)

A report on the surging demand for semiconductor chips produced by S&P Global highlighted a number of key areas responsible for increasing purchases.

According to the company, the demand for electric vehicles increased by 50% between 2019 and 2020, while the demand for 5G smartphones saw an increase of 468%. The personal computer market’s demand levels also grow by 6% between 2019 and 2020.

Statistics on the Effects of the Chip Shortage

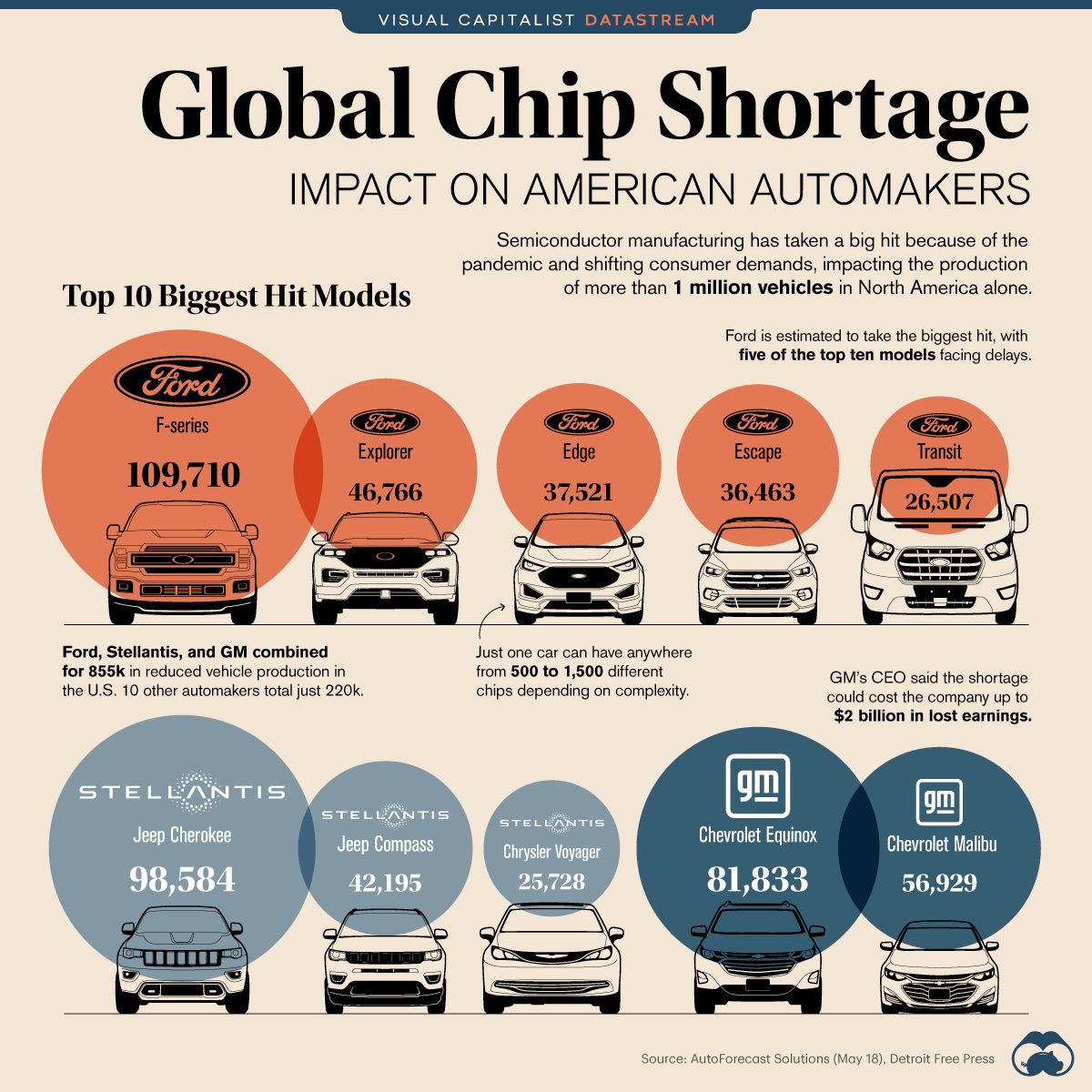

10. Automobile companies will lose $210 billion in revenue in 2021 due to the chip shortage.

(AlixPartners)

The chip shortage is expected to cause a significant financial hardship for the auto industry in 2021 as they will see a decrease in sales and an increase in manufacturing costs.

According to a report by AlixPartners, 7.7 million units of production will be lost due to the chip shortage. This will result in a loss of $210 billion in revenue for the auto industry.

The problem with the chip shortage is that it affects every aspect of the automotive industry. Chips are used in everything from the engine control unit to climate control and security systems.

The chip shortage is likely to continue into 2022 and beyond, as companies scramble to find new suppliers.

11. Median chip inventories have dropped from 40 days to less than 5 days

(Commerce.gov)

Based on 150 responses provided by major auto and semiconductor manufacturers, the US Commerce Department revealed companies are running out of chip inventory supplies much faster as of 2021.

In 2019, the average chip inventory levels were usually around 40 days. However, by 2021, this number had decreased to less than 5 days.

Inventories appear to be particularly short in some key industries, such as the 5G landscape, graphic cards and video game console creation, and gaming PCs.

The Department of Commerce noted a single disruption overseas shutting down a semiconductor plant for up to 3 weeks could immediately furlough workers in the US.

12. Lead times for chips could be 10-20 weeks by the end of 2022

(Deloitte)

A report by Deloitte on the evolving nature of the global chip shortage suggests the issue will continue to persist well into 2023. According to the company, while the problem will still exist in 2023, it may be less severe than in 2020 and 2021.

By the end of 2022, Deloitte predicts most lead times for chips will be between 10 to 20 weeks. This might seem like a long time, but it’s a fraction of what customers were seeing in 2021. The average lead time for some kinds of semiconductors in 2021 was between 20-52 weeks.

13. Around 45% of car consumers are postponing their purchase due to chip shortages

(Cox Automotive)

A report into the impact of the chip shortage on the automotive industry conducted by Cox Automotive found that buyer behaviors are being affected by supply and demand.

The report highlights that new vehicle sales volume had decreased in Q1 of 2022 by 16% from the same period in 2021. This marked the lowest sales volume in over a decade.

According to the report, around one in three consumers now expect delivery of their vehicle to take at least 10 weeks. What’s more, around 45% say they’re likely to postpone their purchase to a time when the chip shortage is less significant.

Of the respondents in the study who said they’d be willing to pay above the average sticker price for their vehicle, most only said they would pay up to 20% more.

14. The chip shortage caused Apple to reduce production of the iPhone 13 by 10%

(Bloomberg)

According to a report issued by Bloomberg, Apple was one of the major telephony companies suffering from the effects of the global chip shortage in 2021.

The report noted that the company had chosen to reduce its production of the Apple iPhone 13 only a month after its release by 10%.

The company announced it was unable to meet with production demands and previous goals because of an inability to access chips from suppliers Texas Instruments and Broadcom.

The report caused significant unrest in the industry, with shares of Apple dropping by around 8%.

Fighting the Chip Shortage Statistics

15. Semiconductor manufacturers are working to boost 200mm fab capacity by 17% by 2024

(SEMI 200mm Fab Outlook Report)

Examining the strategies currently being taken by chip manufacturers around the world, the SEMI 200mm Fab Outlook report suggests companies are aiming to increase fabrication capacity.

Specifically, worldwide producers are on track to enhance 200mm fab capacity by around 950,000 wafers, or approximately 17% by the year 2024.

At the same time, 200mm fabrication equipment spending is reaching new heights. The market value accelerated from $3 billion to $4 billion between 2020 and 2021.

This report also shows that foundries are likely to account for over 50% of fab capacity worldwide this year. What’s more, China will lead the global production efforts, with an 18% market share.

16. The global chip shortage could drive 50% of the top 10 Automotive companies to design their own chips by the end of 2025

(Gartner)

The automotive industry represents one of the most significant landscapes affected by the global chip shortage. According to Gartner’s report into Automotive and Smart Mobility for 2022, the issue is severe enough to convince OEMs to develop their own chips.

By 2025, Gartner believes 50% of the top ten automotive original equipment manufacturing companies will begin designing their own chips. According to the analyst, this will give automotive brands more control over their supply chains and product roadmaps.

The rising demand for chips and innovation from automotive brands may also increase the average price we pay for cars. Gartner’s report also notes the average sale price for new cars in the US is likely to exceed $50,000 by 2025.

17. Since the semiconductor shortage began in 2020, companies have increased their utilization levels to over 90%

(Commerce.gov)

The US Commerce Department published a report in January 2022, highlighting the risks in the Semiconductor and chip supply chain.

According to the report, since the shortage began in 2020, these companies have increased the utilization of their capacity significantly. Between Q2 of 2020 to Q1 of 2021, semiconductor fabricators operated at over 90% utilization.

Notably, the government report highlighted this utilization level is particularly high for such a production process, which is reliant on high amounts of energy usage, and regular maintenance. The report further highlighted this increase in utilization is likely to continue.

18. The chip shortage may not end until some point in 2023

(JP Morgan)

Predictions of when the chip shortage will be over differ depending on the analyst you ask.

JP Morgan’s evaluation of the market suggests the “cyclical” structure of the chip industry will lead to a period of “oversupply” at some point in the future, to balance out the current shortages now.

Looking at the current sales and demand numbers, JP Morgan indicates the earliest time we might start seeing a shift towards an “oversupply” would be at some point in 2023.

The analysts also suggested they believe semiconductor device companies may unlock access to more foundry capacity during the months leading to the end of 2022.

19. The world’s 3 largest chipmakers spent more than $60 billion in 2021

(Deloitte)

According to a report by Deloitte, analysing the statements made by chip manufacturers and semiconductor companies in 2021, huge investments are being made into the industry.

The three largest semiconductor manufacturers in the world spent a combined $60 billion on strategies to respond to the shortage in 2021.

Deloitte believes this amount will increase going forward.

The Deloitte report notes a portion of this spend likely went towards increasing capacity at existing fabrication companies, while some cash may have gone towards construction of new facilities.

For instance, Intel built two new fabrications in Arizona at a price of around $20 billion.

Conclusion

In this article, we have looked at the latest chip shortage statistics so that you can have a better understanding of what is happening and what needs to be done in order to stay ahead of the curve.

Based on the chip shortage statistics that we’ve looked at, it’s clear there is definitely a need for more chip manufacturing capacity.

With continued global growth and demand for semiconductors, producers will need to continue scaling up their production capabilities in order to meet the increasing demand. While things are looking better than they did earlier this year, we will likely see shortages continue for some time to come.

As you can see, the semiconductor industry is in a bit of an upheaval right now. This shortage will likely continue to evolve over the coming years, and businesses that don’t start preparing now could find themselves struggling to keep up.

It will be important for manufacturers and investors alike to stay weathering these supply challenges so that they can fulfill the growing demand for semiconductors.

321 Catchy Metalworking Business Name Ideas

256 Electric Car Slogans and Taglines

23 Tablet Statistics That Are Pretty Surprising